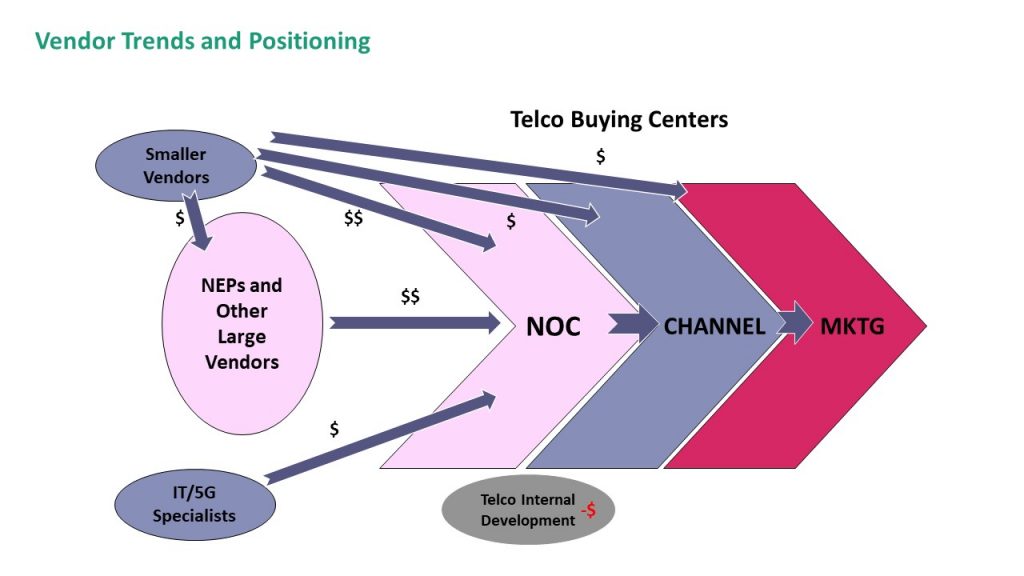

The market is a “red ocean” due to the multiple current and near-term opportunities provided by new 5G networks. As graphically represented below, incumbent vendors still have the “inside track” on the most impactful solutions for the NOC, with smaller players providing a diversity of solutions across the telco using the assurance data set. In future, we expect smaller players to work in a growing number of ways: providing point solution expertise, joining an ecosystem and/or providing capabilities to the bigger players, who do not wish to create a complete product set in certain areas.

Main Findings

- Barriers to sale of more complex assurance capabilities include:

- Key future purchasing departments such as the SOC are relatively small and immature

- The cost and difficulty of implementing new automations, against a backdrop of telco budget constraints

- Going forward, telcos will wish to reuse existing capabilities – although, opinion appears to be that assurance products for physical networks will not be suitable for hybrid/virtual networks

- Some telcos create their own solutions, pushed forward by need for bespoke algorithms that suit their situation, plus corporate level strategy to develop internal data science capabilities. Vendors report that recruitment of data science teams is happening slowly.